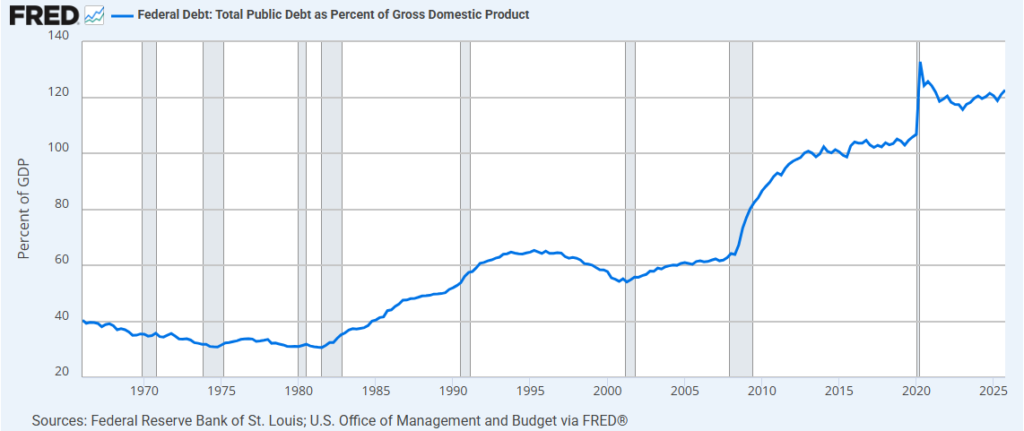

The United States has crossed a historic fiscal threshold: its national debt has now surpassed the size of its entire economy, marking the first time this has happened since the aftermath of World War II. The milestone underscores growing concerns about long-term fiscal sustainability in the world’s largest economy.

The debt-to-GDP ratio—a key measure used by economists to assess a country’s ability to manage its debt—has climbed above 100%, signaling that total federal liabilities now exceed annual economic output. This development comes amid persistent budget deficits, rising interest costs, and increased government spending over the past decade.

Historically, the United States last experienced such levels in the 1940s, when wartime borrowing pushed debt beyond GDP. However, the post-war economic boom rapidly reduced the ratio. Today’s situation is markedly different: instead of a temporary surge tied to a single event, the current rise reflects structural fiscal pressures, including entitlement spending, tax policy, and higher borrowing costs.

The immediate drivers of the surge include pandemic-era stimulus measures, ongoing deficit spending, and elevated interest rates. According to U.S. Treasury data, federal debt has surged past $34 trillion, while nominal GDP stands slightly lower. At the same time, interest payments on the debt are rising sharply, with annual costs now exceeding $1 trillion—making it one of the largest components of federal spending.

Economists warn that this trajectory could limit future policy flexibility. As debt grows, the government must allocate more resources to servicing it, leaving less room for investments in infrastructure, healthcare, or defense. The Congressional Budget Office has projected that, without policy changes, the debt-to-GDP ratio could continue rising in the coming decades, driven largely by aging demographics and healthcare costs.

Financial markets have so far absorbed the increase, largely due to the U.S. dollar’s role as the global reserve currency and strong demand for Treasury securities. However, some analysts caution that sustained high debt levels could eventually lead to higher borrowing costs or reduced investor confidence. A key concern is the feedback loop between interest rates and debt: as borrowing costs rise, they further accelerate debt accumulation.

Not all economists view the situation as immediately alarming. Some argue that as long as economic growth remains steady and the U.S. retains its financial credibility, high debt levels can be managed. They point out that advanced economies like Japan have operated with even higher debt-to-GDP ratios for years without triggering a fiscal crisis.

Still, the political implications are significant. The milestone is likely to intensify debates in Washington over fiscal policy, taxation, and spending priorities. Lawmakers face difficult choices: reducing deficits may require either spending cuts, tax increases, or a combination of both—each carrying economic and political trade-offs.

Looking ahead, the sustainability of U.S. debt will depend on a delicate balance between economic growth, interest rates, and fiscal discipline. If growth outpaces borrowing costs, the ratio could stabilize or decline. If not, the burden may continue to rise, increasing the risk of fiscal strain over the long term.

The crossing of this threshold does not signal an immediate crisis, but it does mark a pivotal moment. It highlights the need for a coherent long-term fiscal strategy—one that addresses structural deficits while supporting economic growth in an increasingly uncertain global environment.